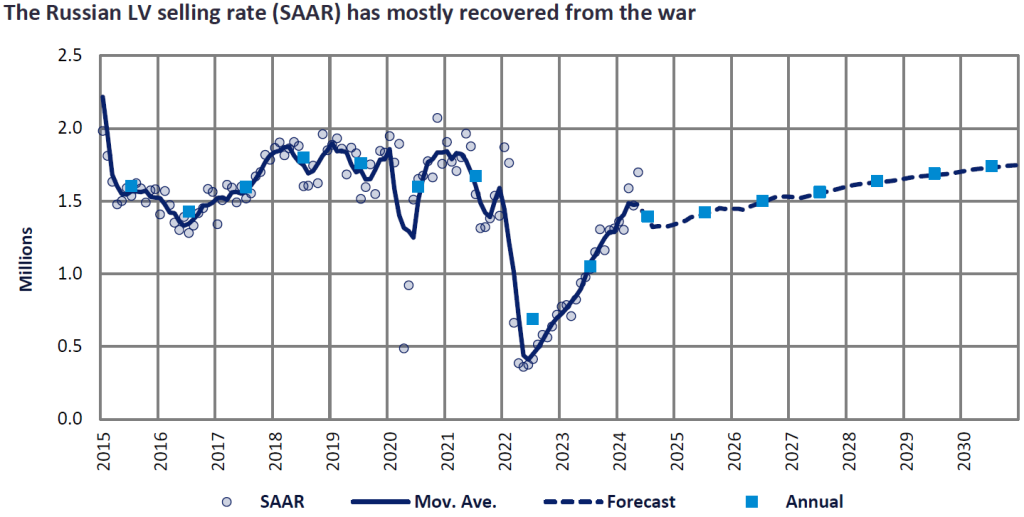

Since it invaded Ukraine, Russia has faced increasing sanctions from its foreign trade partners, particularly the US and Europe. Following the recent announcement of the US Treasury expanding its secondary sanctions programme, international pressure looks set to rachet up even further. However, the Russian economy seems to have broadly adapted to the new geopolitical environment and has seen signs of some recovery. In the Light Vehicle (LV) market, sales volumes are well on the way to recovery – after a near 60% drop in annual registrations in 2022, GlobalData estimates registrations to have grown by as much as 53% in 2023.

The latest estimates for the Russian LV market show that new vehicle sales exceeded 675k units in the first half of 2024 – this constitutes a 78% improvement on the same period last year, an impressive figure compared to somewhat subdued results elsewhere in Europe. While some of this can be attributed to growth in GDP and domestic demand, this result indicates that the LV market has begun to adapt to the sanctions placed on Russia. We do not expect the market to grow as rapidly throughout the year, however, as much of this growth stems from a recovery from the low base of 2023.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

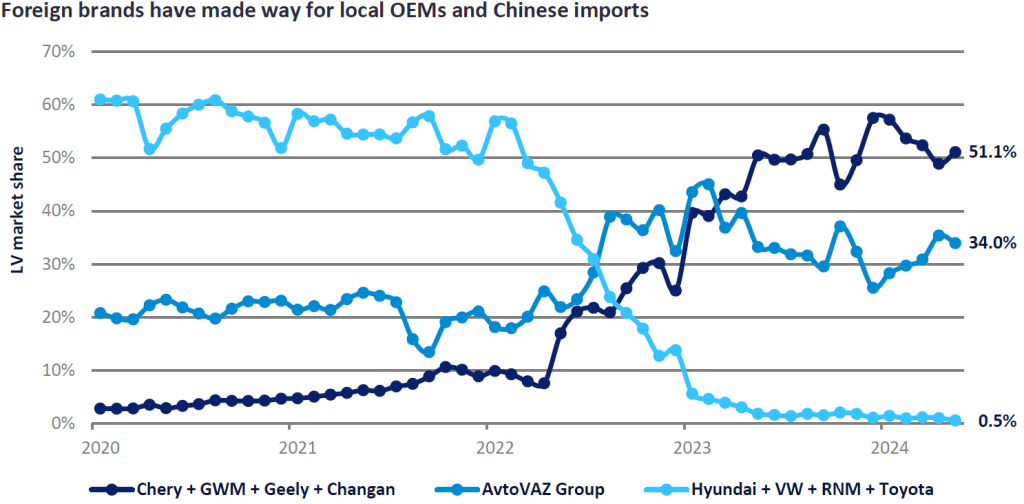

A key component of this remarkable recovery can be examined by considering the entry of new sales groups. Following the invasion, many global manufacturers (including VW, Hyundai, Renault, Nissan, and Toyota) halted production in Russia and began to exit the market entirely. The departure of these brands has created an opportunity for others to seize their market share – the state-owned AvtoVAZ Group, which primarily produces vehicles under the Lada marque, has seen a marked increase in market share since the invasion. Some of this sales growth has been achieved using the assets left behind by foreign OEMs – in February 2023, for example, AvtoVAZ acquired a 99% stake in a former Nissan plant in St. Petersburg.

At the same time, Russia’s close diplomatic ties with China have allowed the entry (and expansion) of Chinese-owned brands such as Chery, Changan, and Great Wall (GWM). As of May 2024, AvtoVAZ retained the highest share of the LV market (34%), followed by Chery Group (19%) and GWM (14%). Volkswagen and Hyundai Groups held second and third places in 2022, but these OEMs exited the market as a result of the war, and only marginal numbers of their vehicles reach Russian consumers today. The influx of Chinese brands and the increase in AvtoVAZ’s sales volumes have allowed the market to recover quickly from the volume losses caused by the conflict in Ukraine.

While partnerships with Chinese and other foreign brands have allowed the market to recover swiftly from the exodus of international OEMs, the future of the Russian LV market is still uncertain. With no indication of a quick resolution to the conflict in Ukraine, it seems that sanctions are more likely to tighten rather than ease – this presents a huge downside market risk. In May, the EU began preparing further sanctions targeting Belarus, to close a loophole allowing Moscow to import luxury cars. This would align the Belarusian sanctions more closely to those already levied on Russia, aiming to eliminate the small numbers of premium Western-branded vehicles circumventing the sanctions. The outcome is uncertain, however, with the possibility of these vehicles reaching Russia through other means.

Looking forward, we expect sanctions to continue to pose a geopolitical risk to the Russian LV market. Many foreign OEMs retained buyback options on their Russian assets – such as Renault, with a six-year buyback option on its majority stake in AvtoVAZ. However, with the conflict in Ukraine expected to continue, it remains unlikely that these companies will return to Russia in the foreseeable future. Following the influx of brands such as Changan, Geely, and Chery to replace the other foreign OEMs, the Russian market has become heavily dependent on imports from China. As such, any future geopolitical flashpoints could still pose a significant downside risk to Russian LV sales.

Ewan McErlane, European Light Vehicle Sales Forecasting, GlobalData

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.