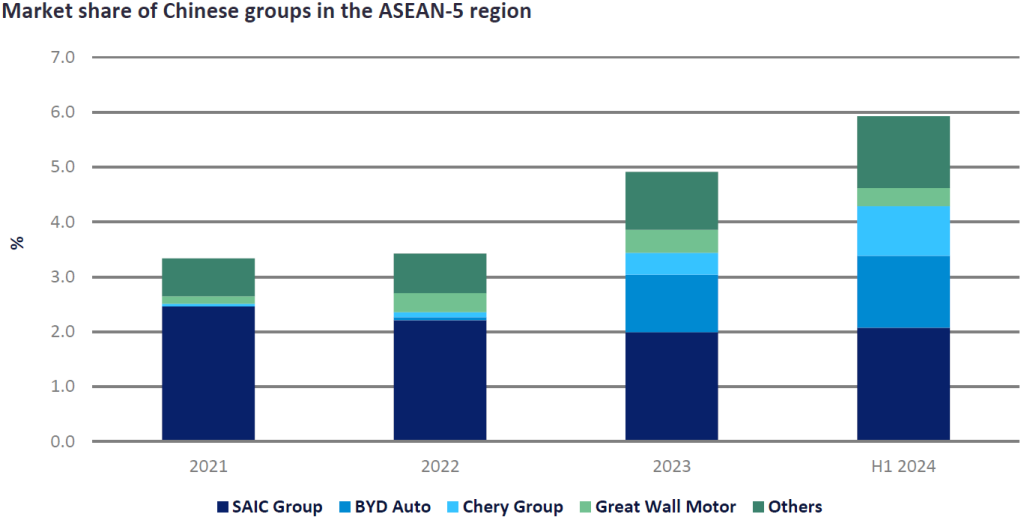

The Chinese brands accounted for 3.4% of ASEAN Light Vehicle (LV) sales in 2021-22. This share accelerated to 4.9% in 2023 and 5.9% in the first half of 2024. SAIC Group was the largest among the Chinese groups in the region. Despite SAIC expanding its model line-up and presence in all ASEAN-5 markets, the group’s market share dropped from 2.5% in 2021 to 2.1% in H1 2024, largely due to a weak sales performance in the Thai market.

Upon closer inspection, BYD Auto and Chery Group were the two main growth drivers for Chinese brands in the region during the previous few years. Combined the two group’s market share was only 0.1% in 2022. However, BYD Auto’s share increased to 1.0% in 2023 and 1.3% in H1 2024, while Chery Group’s share improved to 0.4% in 2023 and 0.9% in H1 2024.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The increasing market success of BYD Auto and Chery Group can be attributed to their entry into new markets and capturing market share from existing players. BYD Auto started operations in Thailand in 2022, then expanded to Malaysia and the Philippines in 2023, followed by Indonesia and Vietnam in 2024. In 2019, Chery Group began operations in the Philippines, followed by Malaysia and Indonesia in 2023, and Thailand and Vietnam in 2024.

With just one brand across all ASEAN-5 markets, BYD Auto saw faster sales and share growth than Chery Auto, even though Chery Auto has four sub-brands: Chery, OMODA, Jaecoo, and Jetour, each of which is positioned differently in different markets. Interestingly, Jetour and Chery are absent from the Thai market, but all of the Chery Group’s sub-brands are active in Indonesia. Jetour is positioned as the most cost-effective brand, while Jaecoo is positioned as the premium brand in relation to Chery and OMODA.

The key differences between BYD Auto and Chery Group are as follows:

BYD began its operations with only Battery Electric Vehicle (BEV) models, while Chery Group primarily focused on non-BEV models. Despite the BEV market being significantly smaller than the non-BEV segment, Chery Auto must compete against established players, particularly dominant Japanese brands. In contrast, BYD Auto operates in a new market that lacks the presence of Japanese manufacturers. Moreover, BEV sales have been boosted by early adopter demand and government incentives, such as Thailand’s cash subsidy programme and Malaysia’s BEV exemption from import tariffs.

Additionally, the segmentation of BYD Auto and Chery Group differs. BYD started with three models in different segments: Dolphin Sub-Compact Car, Atto 3 Compact SUV, and Seal Midsize Car. Meanwhile, Chery Group mainly focuses on the SUV segment in various sizes: Sub-Compact, Compact, and Midsize, with only a Mini BEV car in the Philippines. This could lead to Chery Group’s SUVs cannibalising each other, whereas BYD’s models do not face this issue.

Furthermore, each BYD model targets key segments. For instance, BYD Thailand positioned the Dolphin to compete in the largest Thailand Passenger Vehicle (PV) segment, the Sub-Compact Car or Eco Car. The Atto 3 targets the fast-growing Compact SUV segment, while the Seal directly competes against Tesla’s Model 3.

In Indonesia, BYD promptly launched the M6 MPV to capture market share in the MPV segment, the largest segment in Indonesia. This indicates that BYD Auto understands customer needs and behaviour in each market. Moreover, all BYD models are priced favourably compared to non-BEV models in the same segment.

In an article earlier this year, I mentioned that Chinese brands dedicated solely to BEVs will encounter obstacles in the medium term. While demand for BEV will continue to increase, it will not become the leading propulsion type in the market. Additionally, the number of players is now growing faster than demand. BYD Auto seems to understand this limitation and the pain points for buyers who cannot adapt to owning BEVs, such as charging points and driving range. This led BYD to launch the Sealion Plug-in Hybrid Electric Vehicle (PHEV) in Thailand and the Philippines in Q3 2024. The model is also expected to debut in other ASEAN-5 markets next year. As such, BYD Auto has the potential to grow into one of the top ten best-selling brands in the region after entering the non-BEV segment. Currently, BYD is positioned as the sixteenth top-selling brand in ASEAN in H1 2024.

However, there are several challenges for BYD:

- BYD Thailand reduced the price of the 2023 model year Atto 3 from THB 1.2 million to THB 860k to clear inventory and boost sales. This price reduction strategy could impact brand image, resell value and retention buying, as it could negatively affect future buyers who want to resell the vehicle as a down payment on a new one.

- Aftersales service still needs to be proven. After introducing the Sealion PHEV in Thailand, the company has not yet announced the maintenance costs and details, which are key vehicle ownership considerations.

- Product durability, a strong factor for dominant Japanese brands, remains a question.

- We also expect competing carmakers to re-strategise to counter the fast-growing BYD Auto, not only the Japanese brands but also other Chinese companies.

Titikorn Lertsirirungsun, Senior Manager, Southeat Asia Forecasting, GlobalData

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.