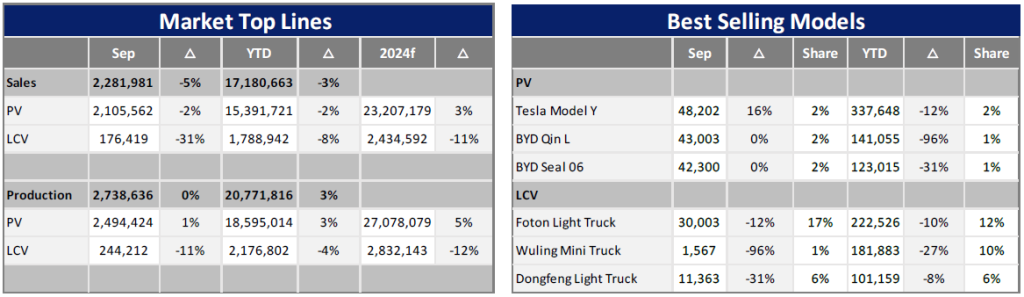

In September 2024, China’s Light Vehicle (LV) market experienced stability compared to the previous month, with sales and production volumes exhibiting divergent trends. Domestic LV sales, excluding exports, reached 2.3 million units, marking a year-on-year (YoY) decrease of 5.4% but a significant month-on-month (MoM) increase of 17.2%. The substantial YoY and MoM differences may be attributed to the high sales base in the previous year and the gradual impact of the old-for-new subsidy policy.

Breaking down the figures by model type, Passenger Vehicle (PV) sales totalled 2.1 million units, with a 2.4% YoY decline but a substantial MoM increase of 18.0%. In contrast, Light Commercial Vehicles (LCVs) also showed a downward trend, which was much more obvious than PV. Although LCV sales increased by 8.4% in September compared with August, they fell sharply, by 31.1%, compared with the same period last year. In the first nine months of 2024, cumulative LV sales reached 17.2 million units, a YoY decrease of 2.7%. Among that number, cumulative PV sales were 15.4 million units, a YoY decrease of 2.0%. LCV’s cumulative sales were 1.8 million units, a YoY decrease of 8.4%.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

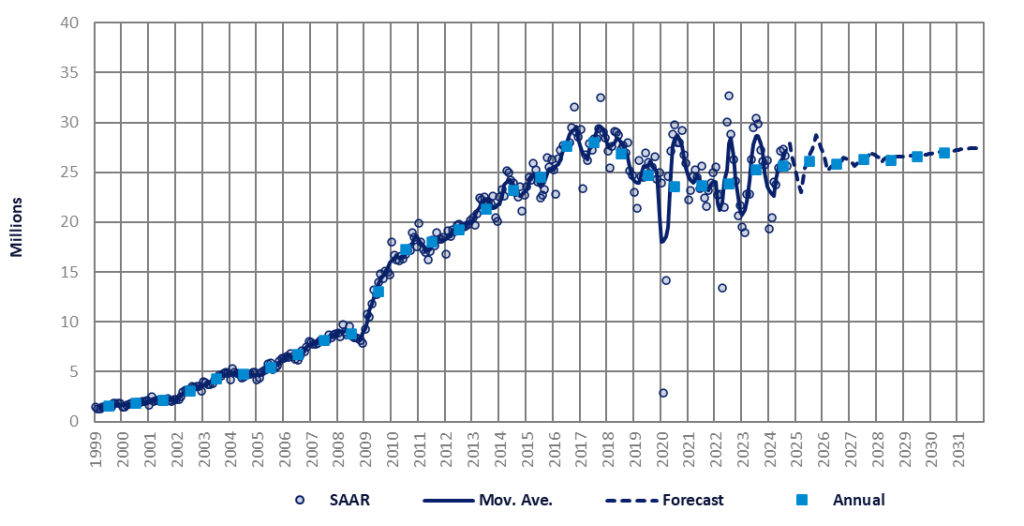

Despite the ongoing scrapping subsidy programme and significant price reductions, the Chinese market slowed for the second consecutive month. The September selling rate was 25.6 million units per year, an almost 4% decrease from August. The YTD selling rate averaged 24.4 million units per year, compared to last year’s total LV sales of 25.2 million units. In YoY terms, sales fell by 6% in September and 2.8% YTD. New energy vehicles (NEVs), predominantly Chinese brands, continued to grow, accounting for 55% of PV sales in September, while sales of internal combustion engine (ICE) vehicles continued to decline sharply.

Seasonally-adjusted annualized selling rate (SAAR) in China

Although the September data fell short of expectations, the third-quarter average selling rate of 26.5 million units per year showed improvement over the second quarter’s 25.4 million units per year and the first quarter’s 21.3 million units per year. Based on the quarterly average, the PV selling rate accelerated in Q3, offsetting the significant slowdown in the LCV sector. It is also important to note that the YoY declines from June to September were influenced by the exceptionally strong sales levels of the previous year. We anticipate that YoY growth will turn positive in the fourth quarter, driven by a lower base and the temporary scrapping subsidy programme.

As of 25 September, according to the China Passenger Car Association (CPCA), over 1.1 million vehicles were registered for scrapping and trading-in on the National Auto Trade-in Platform. The actual number of those that have resulted in new vehicle sales remains unclear. If they all did, it would imply that approximately half of the 2.1 million PV sales in September were subsidised.

With the government recently doubling scrappage subsidies, reducing the required downpayment for automotive financing loans, and planning to gradually lift restrictions on NEV purchases in various regions to boost sales, along with numerous local government incentive programmes, the intense price competition at OEMs and dealerships appears to have reached its limit. This, coupled with several new model launches should encourage consumers to make purchases, leading us to expect an acceleration in sales in Q4.

However, we continue to exercise caution regarding the sales outlook amidst signs of economic deceleration. The GDP growth rate dipped to 4.6% in Q3, falling beneath the government’s annual target of 5% and down from the 4.7% YoY growth recorded in Q2. The downturn in the real estate sector and a lacklustre job market have contributed to a sustained decline in the LCV market over several months. In an attempt to stimulate the economy, the central bank unveiled a broad spectrum of monetary stimulus measures in September. These included interest rate reductions, initiatives to support the ailing real estate sector—such as lowering existing mortgage rates—and financial support to enhance the stock market’s performance. There is an expectation that these measures will contribute to an uptick in economic growth during 2024 Q4. While these actions may help to invigorate consumer confidence and spending, their effect on the automotive sales outlook will be closely observed. The success of the scrappage subsidy programme and other sales incentives will be evaluated in light of these economic initiatives. The Q4 will be pivotal in determining the extent to which the stimulus measures can reverse the current trend and positively influence automotive sales.

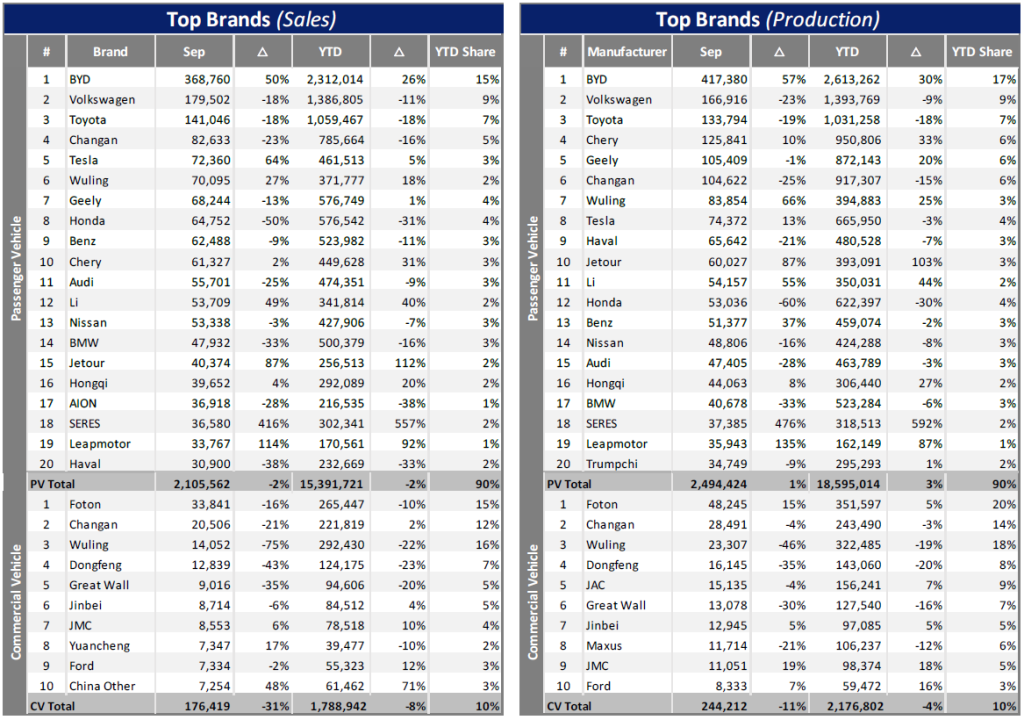

In terms of production, LV manufacturing experienced a slight dip in September, with output falling to 2.7 million units, reflecting a slight YoY decrease of 0.5%. However, there was a notable MoM increase of 12.7%. Over the first nine months of 2024, cumulative production has been robust, amounting to an impressive 20.8 million units, which represents a commendable YoY growth of 2.5%. Breaking down the segment performance, PV production remained stable in September at 2.5 million units, with a minor YoY increase of 0.7%. In contrast, LCV production for September was recorded at 244k units, indicating a YoY decrease of 11.1%. The stability of production levels in comparison to sales can be largely attributed to support from exports. In September, LV exports soared to 522k units, marking a substantial YoY increase of 27%. As the domestic market experiences relatively weak growth, the contribution of exports in propelling production growth has become increasingly significant. This trend underscores the importance of international markets in bolstering the overall performance of the automotive industry.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.