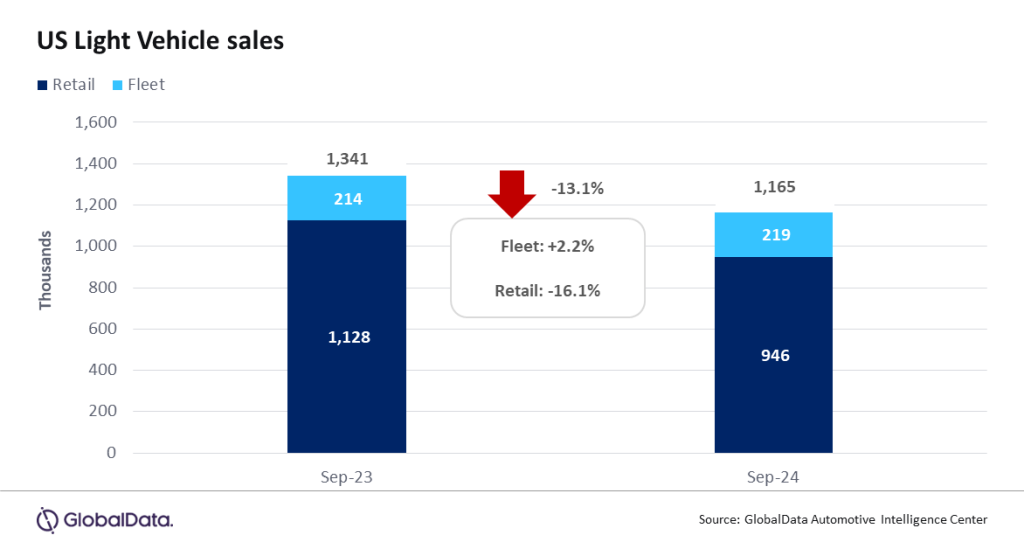

According to preliminary estimates, Light Vehicle (LV) sales fell by 13.1% year-on-year (YoY) in September, to 1.17 million units. As September was shorn of the Labor Day holiday weekend this year, and with only 23 selling days in the month compared to 26 in 2023, the month was always likely to be weak in terms of an unadjusted YoY comparison.

US LV sales totaled 1.17 million units in September, according to GlobalData. The annualized selling rate for the month was 15.8 million units/year, up from 15.2 million units/year in August. The daily selling rate was estimated at 50.7k units/day in September, down from 50.9k units/day in August. Given the quirks of this year’s industry calendar, the factors that raised expectations heading into August – a long month that also included Labor Day – were reversed in September, meaning that forecasts for the month were modest. The annualized selling rate was predicted to rise compared to August, but the fact that the rate ended the month at only 15.8 million units/year – still below our forecast for the full year – indicated a market that is struggling to click into a higher gear. According to initial estimates, retail sales totaled 946k units in September, while fleet sales finished at 219k units, accounting for 18.8% of total volumes.

Go deeper with GlobalData

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

General Motors comfortably retained its position as the leading OEM in September, on 206k units. For the time being, Toyota Group continues to be held back by stop sales orders on the Toyota Grand Highlander and Lexus TX, as well as low inventory levels for the Toyota RAV4. Therefore, Toyota Group’s sales were modest at 163k units. Meanwhile, Ford Group stood in third place with 143k units. Despite the aforementioned challenges, Toyota was still the leading brand in September with 140k units but was only 6k units ahead of Ford. In addition, Chevrolet trailed Ford by fewer than 3k units, the closest it has come to surpassing Ford’s volumes since August 2023, when Chevrolet last finished ahead of its rival.

The Ford F-150 was once again the leading LV in September with 34.0k units, ahead of the Toyota RAV4 on 31.3k units. Even though the RAV4 is being hampered by a lack of inventory, it still beat the Honda CR-V (29.2k units), which had overtaken the RAV4 in August.

After several months in which demand appeared to be easing, Compact Non-Premium SUVs have seen a slight uptick in market share over the past two months, reaching 20.7% in September – its highest since April. In contrast, Midsize Non-Premium SUVs, which had enjoyed a spike in August, fell back to just a 14.5% share in September, the segment’s lowest since December 2019. Large Pickups were not far behind Midsize Non-Premium SUVs in September, holding a 14.3% market share, the best performance for the segment since December 2022.

David Oakley, Manager, Americas Sales Forecasts, GlobalData, said: “September sales were in line with our forecast, although our expectations were modest for what was always penciled in to be a quieter month. Even though the Federal Reserve cut interest rates by 50 basis points – above the expectations of many analysts – it is likely to take some time for lower borrowing costs to feed through to the auto industry. Generally, high vehicle pricing is keeping monthly payments elevated, and therefore some consumers are still sitting on the sidelines. However, leasing deals and heavier discounting for certain Electric Vehicles (EVs) provide the opportunity for buyers to find a bargain, depending on their vehicle needs. Hurricane Helene struck a large swath of the southeastern United States right before the closing weekend of the month, and quarter. Volumes likely would have been marginally stronger without Helene’s destructive presence”.

September inventory levels in the US are expected to rise again as production continues to outpace demand. Volumes are currently projected to increase by 5% from August, with days’ supply remaining in the range of 53-55 days. North American production is now expected to grow by just 4k units, or 0.03%, in 2024 compared to 2023, as the increasing inventory is closely managed heading into the final quarter.

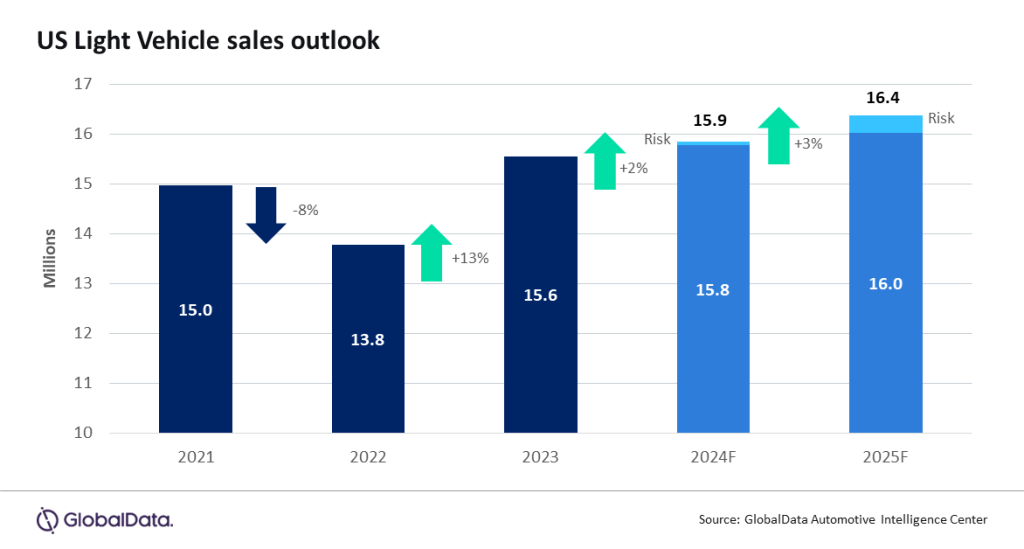

Vehicle demand for the remainder of the year is expected to average a selling rate of 16.4 million units/year, resulting in a forecast that now rounds up to 15.9 million units and represents a 1.9% YoY increase from 2023. Fleet sales are projected to slightly outperform retail sales, with a growth rate of 2.4% YoY, while the retail market is forecast to grow by 1.9% YoY. Auto sales in 2025 are on track to increase by 3.3% YoY to reach 16.4 million units.

Jeff Schuster, Vice President Research and Analysis, Automotive, said: “After another month of steady, yet not accelerating, sales, the halt in robust growth is expected to persist for the next 6-12 months. Our baseline forecast anticipates a moderation in pricing and a decrease in interest rates by 100 basis points or more through the middle of 2025, which should encourage consumers to re-enter the market. However, potential factors such as escalating tensions in the Middle East and the effects of higher oil prices could introduce uncertainty. Furthermore, once the result of the US election is final, we anticipate reduced ambiguity leading to a more positive outlook for auto sales, regardless of the election outcome”.

Global outlook – The global LV sales rate in August remained steady at 89.5 million units, about 300k lower than July, but indicated a stable overall market. The year-to-date (YTD) selling rate has improved to 86.6 million units/year, but volumes are now up just 1% from the same period in 2023. August saw a decline in sales across major markets, with the exception of Brazil and Russia. While volumes in China and North America have remained stable, they are not showing signs of returning to the anticipated growth rate for the second half of 2024. Therefore, the 2024 forecast for global LV sales has been revised down for the fourth time this year, from 89.3 million units at the beginning of the year to 88.5 million units currently. Growth from 2023 has now settled at 2%, driven by elevated pricing, geopolitical risks, and economic performance.

This article was first published on GlobalData’s dedicated research platform, the Automotive Intelligence Center.